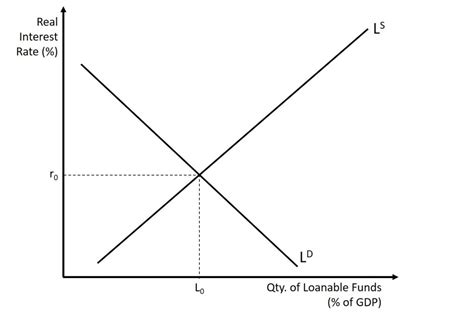

Understanding the loanable funds market graph provides a comprehensive view of how interest rates and the supply of loans interact in financial markets. The loanable funds market, at its core, refers to the market where savings meet investment. Here, the supply of funds is offered by savers, and the demand comes from borrowers. The intersection of these supply and demand curves determines the equilibrium interest rate. This fundamental economic concept is pivotal for policy-makers, investors, and anyone deeply engaged in financial markets.

Key Insights

- The loanable funds market helps determine equilibrium interest rates based on supply and demand dynamics.

- A shift in the supply or demand curve, driven by factors such as monetary policy or economic growth, can cause fluctuations in interest rates.

- Understanding the loanable funds market graph is critical for predicting economic trends and for making informed financial decisions.

Supply of Loanable Funds

The supply of loanable funds is primarily driven by savers who deposit money in banks or other financial institutions. When these institutions lend out money, they create loans. The supply curve in the loanable funds market usually slopes upward. This means that as the interest rate rises, financial institutions are willing to lend out more funds because higher interest rates offer better returns on their deposits. This curve’s slope is influenced by various factors such as interest rate expectations, inflation, and the overall economic environment. For example, during times of high inflation, the supply curve may shift to the left as higher interest rates are needed to offset the eroding purchasing power of money.Demand for Loanable Funds

The demand for loanable funds is determined by businesses and consumers looking to invest in projects or acquire financing for various needs. When firms and households borrow money, they do so to finance capital investments or consumption. The demand curve typically slopes downward, indicating that as interest rates fall, more money is borrowed because lower rates reduce the cost of borrowing. Conversely, higher interest rates discourage borrowing. Real-world instances illustrate this principle; during economic booms, businesses borrow more, shifting the demand curve to the right, while in recessions, the demand decreases, shifting the curve to the left.Equilibrium in the Loanable Funds Market

At equilibrium, the quantity of loanable funds supplied equals the quantity demanded at the prevailing interest rate. The loanable funds market graph plots these supply and demand curves against each other to determine this equilibrium. Changes in either supply or demand will shift these curves, affecting the equilibrium interest rate and the volume of loans. For instance, if government policies induce lower tax rates, thereby increasing disposable income, more people might save and lend, shifting the supply curve to the right and potentially lowering interest rates.How does monetary policy affect the loanable funds market?

Monetary policy, particularly actions taken by central banks like the Federal Reserve, can significantly influence the loanable funds market. By altering the money supply through tools like open market operations, central banks can impact interest rates. For instance, when the central bank buys government securities, it injects money into the economy, increasing the supply of loanable funds, which tends to lower interest rates.

What role does government regulation play in the loanable funds market?

Government regulation, such as reserve requirements for banks, plays a crucial role in the loanable funds market. These regulations determine the amount of funds banks must hold in reserve against deposits, thus affecting their capacity to supply loans. Changes in regulatory requirements can directly impact the supply curve, influencing interest rates and overall lending activity.

Understanding the dynamics of the loanable funds market graph is not only academically significant but also practically indispensable for stakeholders across financial sectors. By analyzing these market interactions, one can make more informed predictions about interest rate trends and economic behavior.