When it comes to understanding the true cost of borrowing money or evaluating the return on investment for financial products, the Effective Annual Rate (EAR) formula is a powerful tool. This formula accounts for compounding interest over time, giving you a more precise picture of the real yield or interest rate. But let’s face it, navigating the world of finance can be daunting. This guide will walk you through the Effective Annual Rate formula in a step-by-step manner, using practical examples and actionable advice. Whether you’re a student, a professional, or simply someone keen to understand their finances better, this guide will demystify EAR for you.

Understanding the Problem: Why EAR Matters

Financial products like credit cards, loans, and savings accounts often have different nominal interest rates that don’t fully account for the frequency of compounding. The nominal interest rate might seem attractive, but it can be misleading without considering how often interest is compounded. This is where the Effective Annual Rate comes into play. EAR gives you the annual interest rate that, if compounded annually, would give the same amount of interest as the nominal rate compounded more frequently. By understanding EAR, you can make more informed decisions on which financial products offer the best value.

The Pain Points

Here’s what you might encounter without understanding EAR:

- Misjudging the real cost of borrowing money.

- Failing to compare the true return on investments.

- Being unaware of how different compounding frequencies impact your savings or debt.

Quick Reference

Quick Reference

- Immediate action item with clear benefit: Calculate the EAR for a credit card with a 15% nominal annual rate compounded monthly to see the real annual cost.

- Essential tip with step-by-step guidance: Use the formula (1 + (nominal rate / number of compounding periods))^(number of compounding periods) - 1 to find EAR.

- Common mistake to avoid with solution: Confusing EAR with the nominal rate; remember EAR provides a more accurate representation of the real rate.

How to Calculate the Effective Annual Rate (EAR)

The formula for EAR is relatively straightforward but essential to understand. Let’s dive into it step by step:

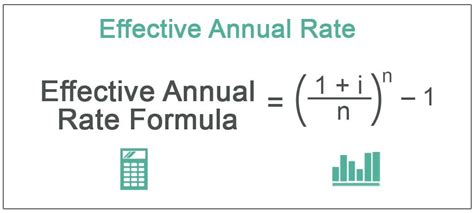

The EAR is calculated using the following formula:

(1 + (nominal rate / number of compounding periods))^(number of compounding periods) - 1

Breaking Down the Formula

To help you understand the formula, let’s deconstruct each part:

Nominal Rate: This is the annual interest rate without considering the effect of compounding. For example, if you have an investment that offers a 12% nominal annual interest rate, this is your starting point.

Number of Compounding Periods: This refers to how many times the interest is compounded per year. Common compounding frequencies include monthly (12), quarterly (4), and daily (365).

Effective Annual Rate (EAR): This is the final rate that reflects the true annual cost of borrowing or the annual return on an investment, considering compounding.

Step-by-Step Example

Let’s walk through an example to solidify your understanding:

Imagine you’re evaluating a credit card with a nominal annual interest rate of 18%, compounded monthly.

Step 1: Identify the nominal rate and the compounding frequency.

Nominal Rate = 0.18 (or 18% expressed as a decimal)

Number of Compounding Periods = 12 (monthly compounding)

Step 2: Plug the values into the formula.

(1 + (0.18 / 12))^(12) - 1

Step 3: Calculate the EAR.

EAR = (1 + (0.18 / 12))^(12) - 1

EAR = (1 + 0.015)^(12) - 1

EAR = (1.015)^(12) - 1

EAR = 1.1956 - 1

EAR = 0.1956 (or 19.56%)

So, the Effective Annual Rate for a 18% nominal rate, compounded monthly, is 19.56%.

Practical Application

Understanding EAR is crucial in multiple scenarios:

- Comparing credit cards: EAR helps you understand which card has a truer cost of borrowing.

- Choosing investments: It allows you to see the true return on different investment options.

- Loan comparison: When evaluating loans, EAR gives a clearer picture of which loan is the most cost-effective.

Advanced Understanding of EAR

Once you’ve grasped the basics, you might want to dive deeper. Here are some advanced considerations:

1. Continuous Compounding: For very small intervals, interest compounds continuously. The formula for continuous compounding is: EAR = e^(nominal rate) - 1, where e is the base of the natural logarithm (approximately 2.71828).

2. Using EAR in Financial Planning: EAR is invaluable for long-term financial planning. Whether planning for retirement, buying a house, or saving for education, EAR helps you understand the long-term impact of compounding interest.

3. EAR in Different Markets: Different financial markets compound interest differently. Understanding EAR can be especially beneficial in comparing international investment opportunities.

Practical FAQ

What is the difference between EAR and nominal rate?

The nominal rate is the annual interest rate without considering the effect of compounding. EAR, on the other hand, accounts for the compounding frequency and provides a more accurate annual interest rate. Essentially, EAR represents the real annual rate if the nominal rate were compounded annually.

How does more frequent compounding affect EAR?

More frequent compounding generally results in a higher EAR. This is because the interest is being calculated and added to the principal more often, leading to more interest being earned over the same period.

Why is it important to understand EAR when choosing investments?

Understanding EAR allows you to compare the true return on different investment options. It’s a more accurate way of evaluating which investment will yield the best return over time, considering the effect of compounding interest.

By understanding and applying the Effective Annual Rate formula, you can make more informed financial decisions that align with your long-term goals. From comparing the cost of different loans to maximizing your savings, EAR is a crucial tool in your financial arsenal.